Affordable Life Insurance For Everyone.

If your family depends on your salary, life insurance is a critical piece of making arrangements for your family's future. It's bleak, and nobody likes to get ready for their passing, however a little uneasiness presently can spare your family a universe of monetary pressure should the most noticeably awful happen.

The two main types of life insurance are term and whole life. Whole life is in some cases permanent life insurance, and it incorporates a few subcategories, including traditional whole life, universal life, variable life and variable universal life.

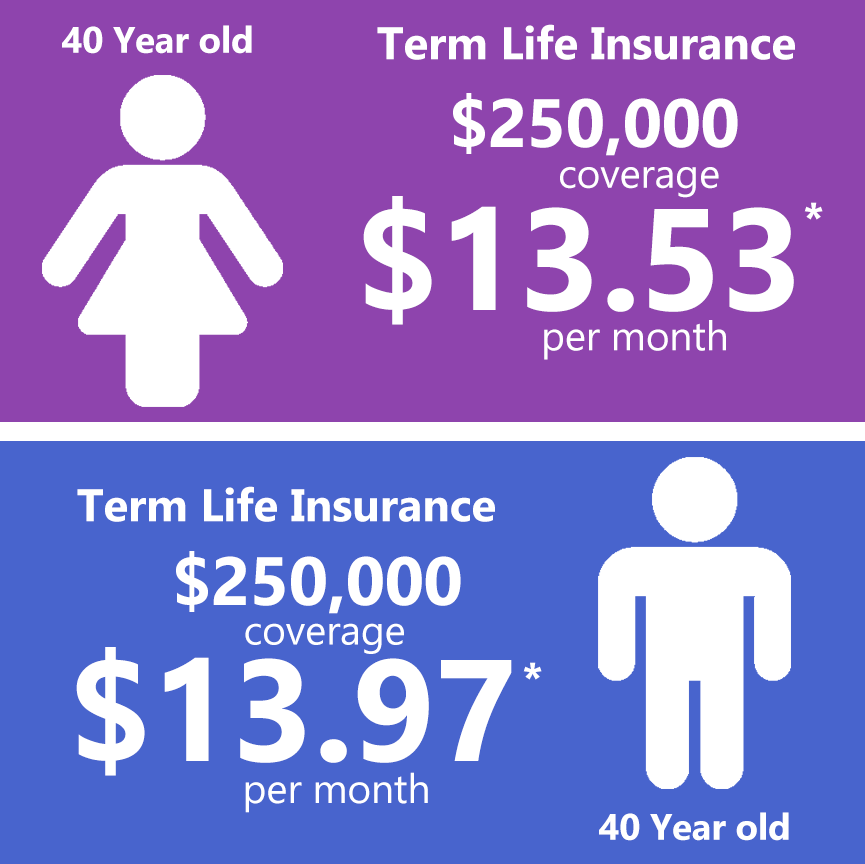

Term Life Insurance

*These rates are for a 40 year old healthy nonsmoking female and male buying a 10 year “Term Life Insurance Policy”. These rates may vary depending on your age, duration of term and other risk factors.

Term Life Insurance can now be had for as little as $15 per month.

Term Life Insurance is extremely popular since it is one of the least complex and most affordable Life Insurance products available. When death occurs, the deceased beneficiaries get paid money if it was during the term of the policy, which is usually between one and 30 years.

There are two basic types of Term Life Insurance level term and decreasing term. Level term means that the death benefit stays the same throughout the duration of the policy. Decreasing term means that the death benefit drops, usually in one-year increments, over the course of the policy’s term. To find out more information request a quote today.

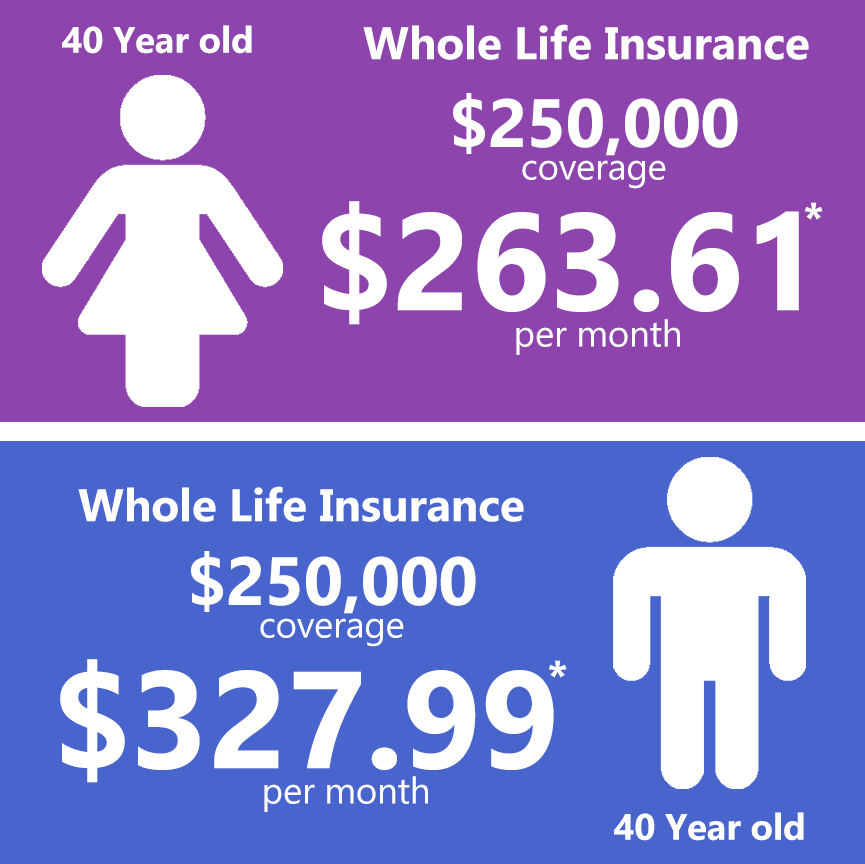

Whole Life Insurance

Whole life or permanent insurance pays a death benefit at whatever point you kick the bucket—regardless of whether you live to 100! There are three noteworthy kinds of Whole life or permanent life insurance— traditional whole life, universal life, and variable universal life, and there are varieties inside each sort.

On account of traditional whole life, both the death benefit and the premium are aimed to remain the same (level) for the duration of the policy. The cost per $1,000 of benefit increases as the protected individual ages, and it gets higher when the person lives over 80 years old. The insurance agency could charge a premium that builds every year, except that would make it difficult for the vast majority to manage the cost of life coverage at cutting edge ages. So the company keeps the premium level by charging a premium that, in the early years, is higher than what's expected to pay claims, investing that money, and after that utilizing it to supplement the level premium to help pay the cost of insurance for older individuals.

By law, when these "overpayments" achieve a specific sum, they must be available to the policyholder as a cash value on under the policy. In the 1970s - 1980s, life insurance organizations announced two variations from the customary whole life product— universal life insurance and variable universal life insurance. To find out more information request a quote today.

*These rates are for a 40 year old healthy nonsmoking female and male buying a “Whole Life Insurance Policy”. These rates may vary depending on your age and other risk factors.